The Queen’s administration releases regular updates on projected budget deficits, but it’s the end-of-year audited financial statements that provide the clearest picture of the university’s financial health. With the Board of Trustees meeting this weekend, those figures have now been released.

The 2023-24 financial statements are interesting for several reasons, but one figure stands out: A year-end operating budget surplus of $20.4 million (and an overall surplus of $76.2 million).

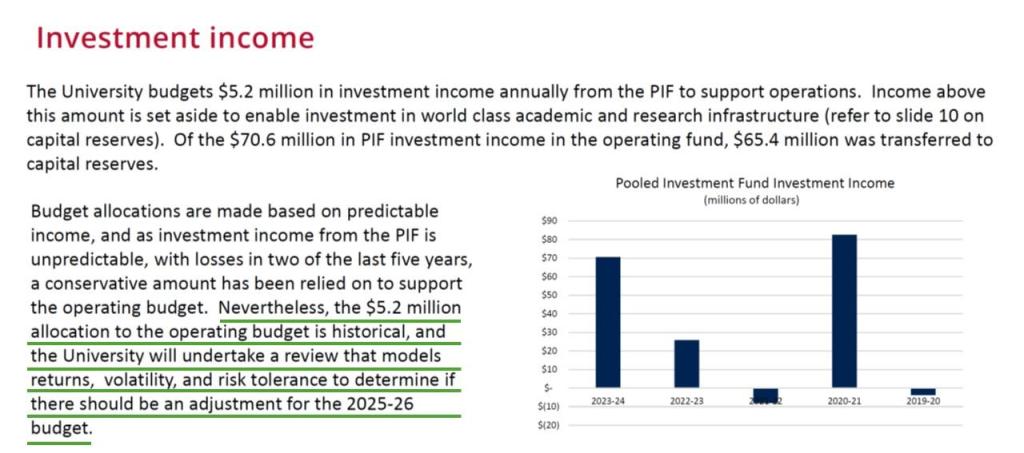

The operating surplus was driven by $89 million derived from investment income, which included $70.6 million from the university’s Pooled Investment Fund (PIF). Dashing any hope that these funds might be used to avert further spending cuts and job losses, the administration chose to transfer $65.4 million of this amount to its capital reserves, making a total of at least $100 million that has been moved from operating to capital over the past two years.

This means that Queen’s’ internally restricted funds (i.e., non-endowment funds) grew from $389.6 million to $405.5 million while the administration sent message after message about the dire state of its financial picture. This total includes $111 million in capital reserves not allocated to any project.

To square this circle, the university has had to get innovative with its accounting practices. A new category titled “Operating deficit before investment income and one time STEM grant” is used to present a “deficit to be addressed” that ignores investment income and some provincial funding to present a case for austerity.

The administration justifies this presentation of its financial picture with arguments that since the STEM grant of $10.7 million was a one-time payment and that investment income fluctuates (see our previous discussion of this argument here) there is incontrovertible proof of the need for cuts. However, one could easily treat fluctuating expenses in the same way to make the opposite argument. For instance, transfers from operating to capital within the operating budget (so outside the PIF transfer) included $25 million for renovations to Duncan MacArthur Hall. This expense was likely a one-off (like the STEM grant) since the project is due for completion in 2025, but we don’t see an equivalent category denoting “Operating surplus before one-time transfers to capital” used to argue that the surplus is closer to $45 million. Perhaps it’s best to stick to the standard accounting entries in future reports?

In better news, the update makes clear that ongoing resistance against the budget crisis narrative has produced some positive results. The report acknowledges that limiting the use of PIF investment income for operations to $5.2 million is “historical” (i.e., arbitrary) and that the administration will review this practice.

QCAA hopes this means that more money can be invested in the university’s academic mission. While it is prudent not to rely on large-scale investment returns, presuming minuscule yields is not good practice either, especially when the quality and reputation of the institution are at stake.

The budget pressures facing Queen’s are real, and provincial policy means that revenues are not keeping pace with inflation. However, decisions about how to use the university’s considerable wealth are political, not inevitable. By every measure reported in its year-end statements, Queen’s outperforms the financial thresholds recommended by the Ministry of Colleges and Universities.

Yet the administration is clinging stubbornly to its austerity plan, presenting an overview of its accounts that obfuscates its choices and lays the groundwork for further cuts.

Let’s not forget that there is room to maneuver here, to make different decisions, and to support the university’s academic mission through this challenging period. And let’s use every opportunity we have to remind one another and our leaders that another path is possible.