On May 15th, the Gazette published a statement about the 2023-24 fiscal year and the upcoming 2024-25 budget for the university. In this statement, administrators outlined arguments regarding the university’s fiscal planning. Here, we address some points that are worth further discussion.

Using investment income: A middle ground and something the university is doing

The university has consistently argued that it would be unwise to use investment income for operating due to market volatility. However, this argument (1) dismisses a more nuanced discussion of how to plan for an increased, but sustainable, use of investment income and (2) is undermined by the fact the university is proposing to increase its use of investment income for operating costs next year (which is good!).

We elaborate on both points:

- The outright dismissal of a discussion around investment income misses the middle ground between using all investment income and planning to use more investment income sustainably.

As we have documented, the amount of investment income the university plans to use from the Pooled Investment Fund (PIF) has remained the same since 2016-17. This is despite the fact that the fund has more than doubled in value over this time. Freezing the budgeted use of investment income at 2016-17 levels has resulted in a functional decrease in the percentage of PIF investment income used for operating expenses. The university has never explained the logic of not adjusting the use of investment income from the PIF in accordance with the fund’s growth to maintain a sustainable but growing contribution to operating. The figure below illustrates this dynamic and its effects:

- All that being said, the university is planning on budgeting for more investment income next year!

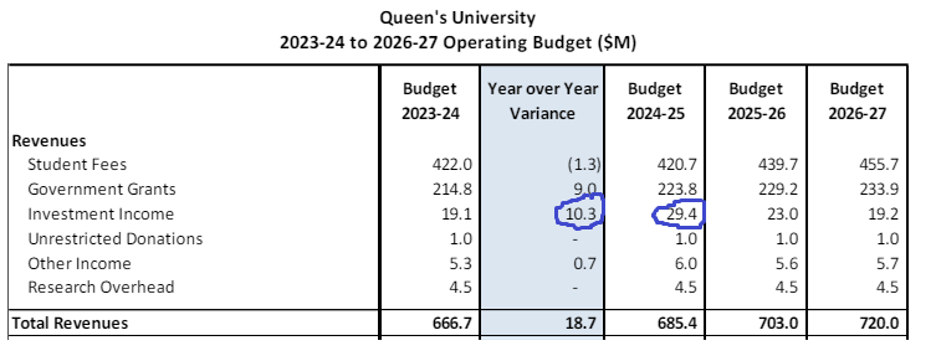

As laid out in the projected 2024-25 budget presented to the Board of Trustees, the university has taken our advice and decided to allocate an additional $10.3 million in investment income to the operating budget next year, raising that figure from $19.1 million to $29.4 million (see figure below). As they describe on p. 80: “Additional funding has also come into the University Fund due to short-term investment income, which we are budgeting to increase by $11 million in 2024- 25.”

The administration does state that this additional investment income will be placed in a ‘contingency fund’ that they have not decided how they’ll use. As they describe, having this unallocated fund in the budget is a means of adjusting for the supposed uncertainty of these investment returns. We’re glad the university has started to figure out new ways to use its considerable financial resources to support the operating budget, despite its messages in the Gazette stating otherwise. We’d suggest they could do more but at least they are showing openness to using investment income to support operations when it does materialize rather than transferring it all to capital.

Digging into the details, this increased investment income is likely coming from the Short-Term Fund rather than the PIF (although we cannot confirm this). The Short-Term Fund is another investment fund held by the university, which is used to invest money the university may need on a short-term basis. Unlike the PIF, the Short-Term Fund’s contributions to operating are not limited to a set amount (there is no equivalent to the $5.2 million cap). The budgeted increase in investment income used for operating costs in 2024-25 may therefore be driven by the decision to transfer $200 million from the PIF to the Short-Term Fund in March 2024 (p. 38).

What are we talking about when we talk about volatility?

The university repeatedly argues that the use of investment income needs to be restricted because of the risk presented by market volatility. To make this point, recent communications have informed us that the PIF has suffered losses in two of the past four years. That is true, but some important context is missing here.

While administrators highlight these losses, they do not mention the fact that these recent losses have been quite small while investment returns have often been significantly larger (see figure below). This is demonstrated by the close to $70 million return from the PIF that is projected this year and the similar return from 2020-21. The combination of large returns and small losses provides room to smooth out the flow of income into the operating budget. For example, this year’s projected return would provide enough money to sustain a $5.2 million payout yearly for over a decade.

Source: 2023-23 Audited Financial Statement

Further, it should be noted that the volatility of the Pooled Investment Fund is also partly a choice the university has made. As described in Queen’s Statement of Investment Policies and Procedures, the money in the PIF has been invested in a manner that seeks to ‘maximize medium-term nominal returns.’ This means the university has chosen to accept a higher level of volatility to maximize the investment income it will receive over a longer-term horizon rather than focus on returns on a year-to-year basis.

In contrast, the Short-Term Fund is designed “to obtain a reasonable level of return commensurate with a low-risk, highly liquid portfolio.” It, therefore, produces a safer but likely smaller return. There are pros and cons to each approach but, again, this context is important.

Can we stop with the household comparisons? Why the RRSP argument makes no sense

In explaining the decision not to use investment income for operations, Donna Janiec, Vice Principal of Finance and Administration, offers a household budgeting analogy in the statement in the Gazette, saying you would not draw on your RRSP income to handle household expenses. In general, any comparison between household finances and those of an institution that can issue bonds and has 100s of millions of dollars in revenue will be misleading, but this one is especially strange.

The reason not to draw on an RRSP is because you’ll need the income it can provide when you retire and are earning less income. The university is not going to retire and stop raising revenue, which raises the question of what its savings are for? You’ll remember that at the special Senate meeting on the budget, Donna Janiec mentioned new buildings as the main reason for saving investment income.

If we are forced to belabour the domestic metaphor, her comment prompts a further question of why one would forego spending on the things one needs to live – food, heat, warm clothing – to save for a nice-to-have purchase. Perhaps the better metaphor here would be cutting back on your food budget (the essentials that make it possible for the work of the university to get done) to preserve your savings for a new deck. Of course there are problems with this comparison as well, which just highlights that these types of examples don’t work and we should leave them in the dustbin.

One thought on “A critical read: Providing context for the University’s budget announcement”